CAP-XX

Will this capacitor manufacturer supercharge your portfolio? or run flat like a dead battery...

Is CAP-XX a revolutionary technology company patiently waiting for its moment in the sun? Or just another zealous destroyer of wealth lurking in AIM’s dark corners? I’ll explore this Australian supercapacitor designer and manufacturer, recently revitalized by a new management team, and ask—can they turn this 20-year-old company around?

Capacitors on steroids

Capacitors are boring. Capacitors are cheap, standard electronic components that get investors’ pulses racing like the 40-year JGB. While ubiquitous in modern circuitry, they retail for a few cents apiece.

Supercapacitors are exciting. They have ‘super’ in the name. Supercapacitors have thrilled investors for years, pitched as a disruptive energy-storage technology. Though the idea that they could replace lithium-ion batteries is far-fetched, their relatively high energy density and fast charging kinetics make them useful auxiliary components in modern circuits.

CAP-XX was founded in 1996 to commercialize the research of the Australian government agency CSIRO1. CSIRO’s innovations through the 1990s underpin the technology for small, thin prismatic supercapacitors (prismatic referring to their rectangular form factor). The company floated on the London Stock Exchange in 2006, raising A$37.5m2 under the guidance of CEO Anthony Kongats. This was the peak of the mobile phone revolution and the age of the portable music player—technology promising smaller, fast-charging personal devices was a natural sell.

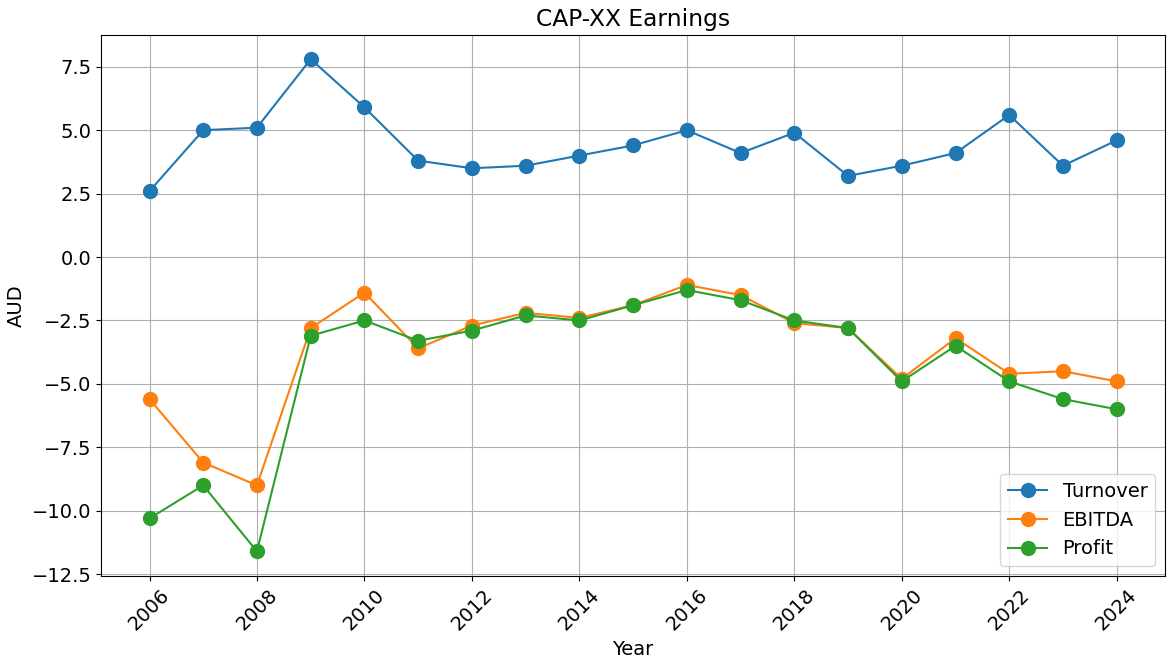

Things got off to a good start. The company pursued revenue generation through both direct product sales and IP licensing—deals followed with industry heavyweights Murata3 (in 2008) and AVX4 (in 2016). Despite the early optimism, the widespread adoption of supercapacitors in portable consumer electronics failed to materialize. CAP-XX revenues remained flat, largely stuck within an A$2-5m range while consistently making a loss:

Things go wrong(er) for CAP-XX

A decade of losses would make any investor feel queasy, but things were about to get worse. In 2019, Murata exited the supercapacitor market5, depriving CAP-XX of a key revenue stream. The company made the bold decision to acquire Murata’s production lines and bring manufacturing in-house, raising £3.42m6 and shipping the lines to a new facility in Seven Hills, Sydney. The number of retained Murata customers is unclear, but was forecast by CAP-XX at 75% in 20227 with CAP-XX suffering lost revenues in the interim.

The AVX licensing agreement began with promise, an A$1m signing fee and early revenues in the six-figure range. However, by the early 2020s, the relationship had become strained. CAP-XX complained that AVX was failing to pay due royalties8 and started legal proceedings that were settled in 2024, with both sides paying their own costs9. A second valuable revenue stream had been lost.

Throughout this period, CAP-XX pursued an aggressive legal strategy that, while successful in some cases (a 2020 ruling against Ioxus awarded CAP-XX $4.95 million10) was not without risk. In 2023, a protracted lawsuit against Maxell Technologies (acquired by Tesla in 2019) culminated in the invalidation of two of CAP-XX’s patents11. This left the company with pronounced cash-flow issues in 2023 and raised serious questions about the strength of its IP protections.

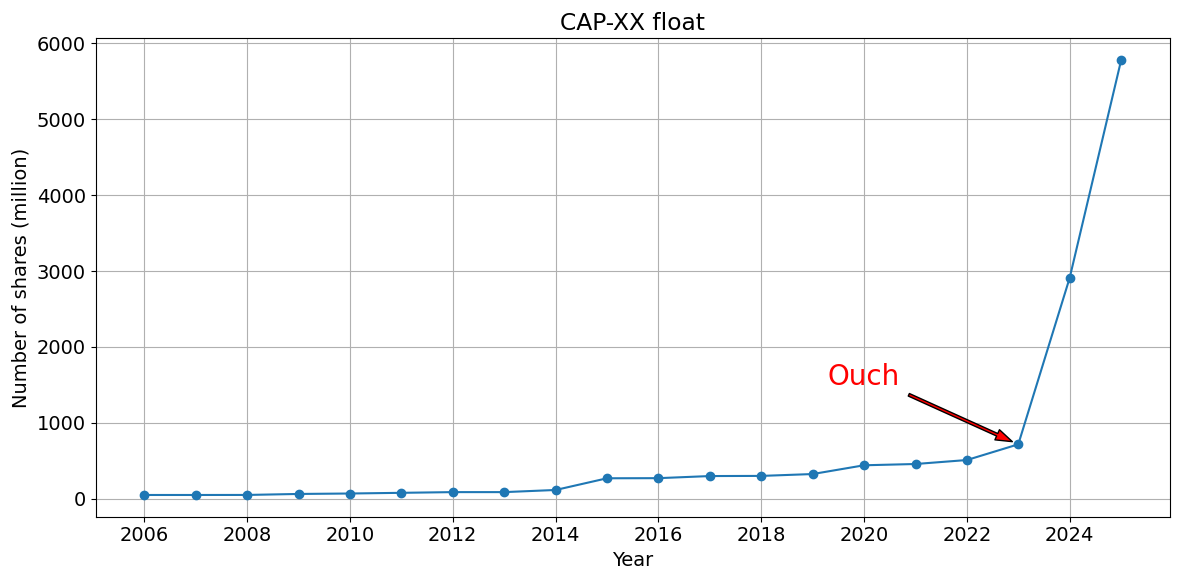

Say what you will, a business that manufactures advanced electronic components as a loss-leader to front risky IP lawsuits is certainly novel. Two eye-wateringly dilutive issuances in 2024 added over 4 billion shares12,13 (from a starting point of ~700 million), raising a combined £4.5 million.

The bull case

Take their stock, put in the timeframe all. They have lost 99.79% of their value. That’s the most I’ve ever seen without a company actually dissolving to nothingness. So in that sense it’s pretty damn impressive.

But why the f*ck would you ever invest in it?

Reddittor, 2024.

In May 2023, CEO Anthony Kongats stepped down from CAP-XX, ending his 27-year tenure14. Since then, many C-suite and board members have left the company. Their stewardship of CAP-XX was exemplified by strong technological competence, but impeded by questionable commercial strategy. The bull case is that the strong technological foundations are now ripe for exploitation by a business-savvy management team.

The new management team, recruited since mid-2023, includes CEO Lars Stegmann, formerly of Molex and C&K. Entrepreneur Graham Cooley, known for his fundraising success at ITM Power, joined as chairman, having made a significant personal investment in the company.

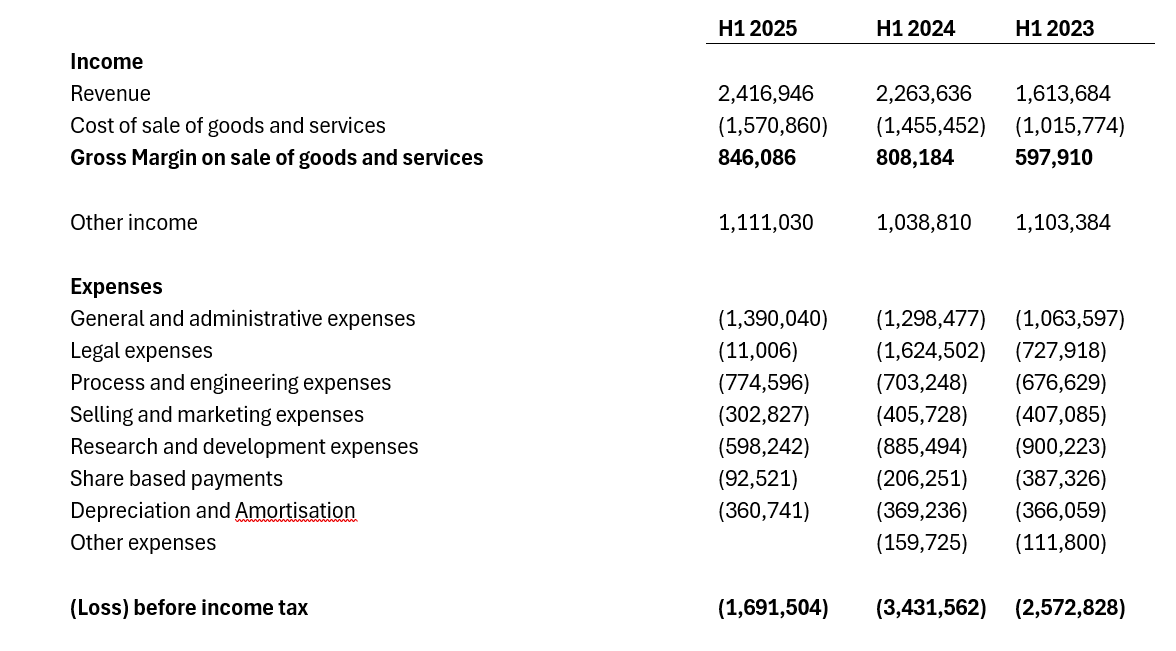

It is difficult to argue with the sensible approach taken by new management. Outstanding lawsuits have been settled and the licensing model scrapped. Instead, there is a strong focus on revenue growth through product sales (FY2024 revenues from direct sales were up 39.7%15). The distributor network is being extended, with CAP-XX products now available from global suppliers including Farnell, RS and DigiKey. Cost-cutting measures have been executed while CRM, accounting, and MRP have been modernized16 and the sales team expanded17. The company is targeting breakeven by 2026, as stated in the H12025 earnings call.

Keeping up the momentum, CAP-XX signed a Memorandum of Understanding with leading electronics manufacturer SCHURTER18, promising collaboration on future product development. Significantly, SCHURTER will leverage their large distribution network to sell SCHURTER-branded CAP-XX supercapacitors19. In January 2025, the first shipment was delivered, solidifying this key revenue stream.

Finally, there is the “game-changer” (2023 RNS20) innovation in the R&D pipeline (these always get AIM investors’ blood pumping). CAP-XX has, for over a decade, been working on a surface-mount technology enabling its cylindrical supercapacitors to withstand reflow soldering. Most circuit boards are soldered using high-throughput reflow ovens, but standard supercapacitors cannot tolerate the heat. Instead, they are often hand-soldered, a costly and time-intensive process. CAP-XX appears close to rolling out this exciting technology, which would expand its market reach and generate immediate revenues.

Bull in a China Shop

Superficially, the bull case is enticing. In classic AIM-investor fashion I was initially so taken by the thesis I immediately invested (at the ‘bit-more than wise’ level). However, I soon scaled back significantly. For me this stock was a ‘reverse Berkshire’, the more I read about CAP-XX the less I want to invest.

The bull case rests on CAP-XX breaking even by 2026, as targeted by management on the H12025 earnings call. The stakes couldn’t be higher. If breakeven is not achieved before cash runs out, another heavily diluting re-raise is inevitable.

Let’s look at CAP-XX’s H12025 earnings to determine the scale of the task at hand. How much do revenues need to grow to hit breakeven?

Gross margin is 35%, with a loss (excluding depreciation and amortization) of $1,330,763. To cover this loss, CAP-XX must generate additional half-year revenues of A$3.8 million, with total annual revenue needing to reach A$12.2m. This is 2.6x full-year 2024 turnover and 1.5x their highest-ever year (A$7.8m in 2009). While management has had only a year to build their strategy, revenues in H12025 were just 6% higher than H12024.

Can the focus on cost-savings lower the bar for revenue growth? CAP-XX reports a 30% reduction in operating costs in H12025 earnings, but these appear to come from R&D and sales and marketing. Cost of sales (at approximately 90% direct materials and labor), administrative, and process and engineering costs are fairly static year-on-year. Further cost reductions appear unlikely, given the expertise and quality of materials required in supercapacitor manufacturing and that the majority of restructuring costs were planned for FY2024.

Notably, around A$1m per half-year of ‘Other income’ is a tax credit courtesy of the Australian government’s R&D Tax Incentive scheme. Excluding it, CAP-XX would need to generate additional revenues of A$6.5m for the half year and nearly quadruple current sales. Notably, the tax incentive scheme is currently under strategic review21, though there is no indication it will be discontinued.

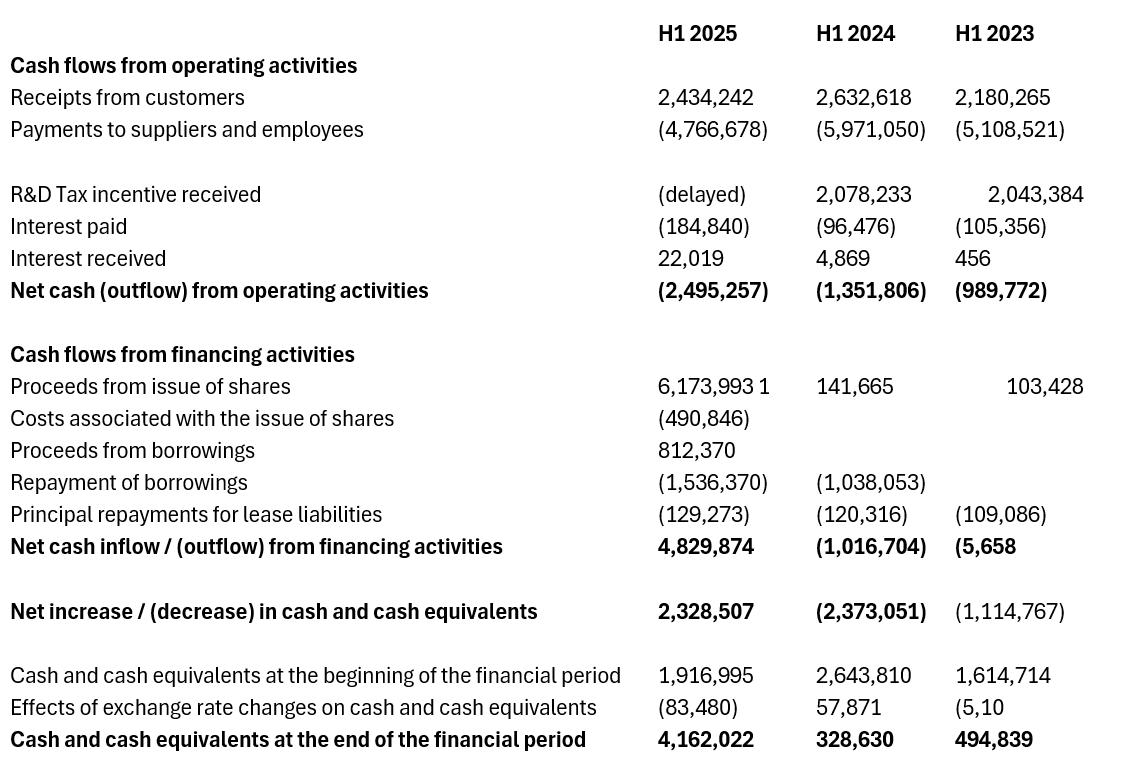

It would be fair to describe CAP-XX’s cash flows, above, as ‘precarious’. The company's current cash reserves are insufficient to cover its half-year outgoings, with the company heavily reliant on the R&D rebate. While access to a credit facility (collateralized by the rebate) provides flexibility, delays in invoice payments could quickly cause cash flow issues before breakeven is possible.

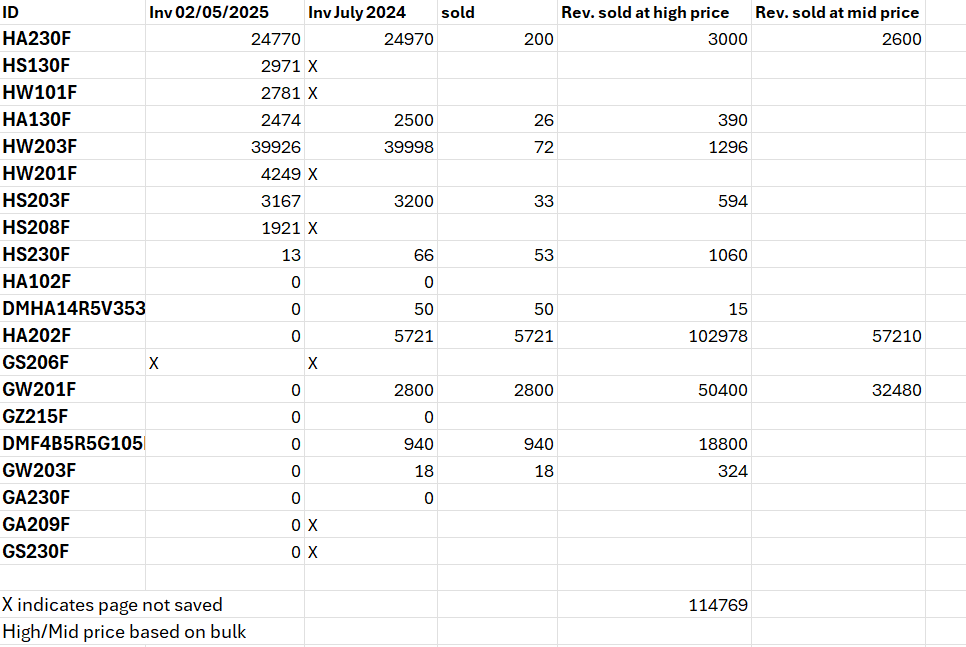

Now, let us dabble in the dark art of earnings estimation and attempt to divine progress towards 2026 breakeven. Two new revenue streams flow from the distribution deal with DigiKey, and sales of SCHURTER-branded supercapacitors. First, I compared recent and past stock levels on the DigiKey website using the WayBack Machine. This gives a revenue estimate of around A$200k to A$300k since July 2024 (though this could be higher, see Appendix I for caveats).

Billings from the first SCHURTER shipment were realized in January 202522, with revenues up 62% year-on-year at A$321k. This suggests A$122k was netted from the SCHURTER shipment, assuming stable underlying sales. SCHURTER-branded supercapacitors have now started appearing on distributor websites. It is unclear when the next shipment will occur; however current distributor stocks indicate repeat orders seem unlikely in the near term.

The decision to sell SCHURTER-branded supercapacitors is a curious one. SCHURTER-branded CAP-XX supercapacitors now appear for sale on the very distributor networks that CAP-XX has spent the last year courting. These identical capacitors (with equivalent specs but different branding) are listed side-by-side with CAP-XX products. This new revenue stream, while welcome, will cannibalize CAP-XX’s existing sales.

These estimates, even if wrong by some margin, suggest new revenue streams will not get CAP-XX within reach of breakeven. Will a large contract win provide the much-needed sales? Recently, CAP-XX announced a contract win (Oct 202423) and a design win via a Reach RNS (May 202524), though details remain confidential. Given the task at hand, only two such announcements do not inspire confidence. These would have to generate significant revenues to move the needle on breakeven, likely larger than any contract CAP-XX has booked in over 20 years of business.

A fundamental problem

CAP-XX has been selling prismatic supercapacitors for a long time. Since 2006, revenues have remained flat while manufacturing giants like Murata have strategically exited the prismatic supercapacitor market. This is despite the overall supercapacitor market growing from approximately $20 million in 2006 to $2.94 billion in 202425,26. Clearly, CAP-XX’s niche is not growing.

This indicates an inherent problem with the CAP-XX product line. The raison d'être of CAP-XX’s small-form prismatic supercapacitors is for mass-market consumer products. As noted in the 2006 annual report: “In 2004, approximately 900 million portable electronic devices were sold, including over 600 million mobile phones… and MP3 players. Many of these devices could benefit from supercapacitors”. A similar vein is mined today with references to the “internet of things”. The core contradiction is that prismatic supercapacitors are prohibitively expensive for such mass-produced consumer products. Whereas coin cell supercapacitors are priced around $1 (and standard supercapacitors on the order of cents), prismatic supercapacitors are in the range of $7-8.

This disconnect is likely the reason for persistently sluggish sales and low revenues. Designers will look long and hard for a cheaper option before committing to such an expensive component. This would explain the curious observation that while the North American sales team was expanded in late 2023, US sales actually decreased year on year by H12025. No management team can revitalize a business if the fundamental problem is the product.

Does the game-changing surface mount technology offer a glimmer of hope? Unfortunately, this may not be as revolutionary as first appears. KEMET’s FC-series, already available for sale, are reflow-oven compatible coin cell supercapacitors in the 0.1-1F range27. CAP-XX’s SMT would appear to have the edge (assuming it is successfully brought to market), covering an extended 0.1-20F range with its reflow compatible cylindrical supercapacitors. Nonetheless, this certainly takes the shine off SMT’s potential, and it is not clear that even SMT could generate the significant revenues required for breakeven before 2026.

The Verdict

Prediction: CAP-XX will run out of cash in 2026, attempting to raise further capital with issuance of around 2.5 billion shares (assuming A$5m, ~£2.5m at share price of 0.10p). This would be around a 30% dilution to the current float. If successful, it is hard to imagine the trick would not need to be repeated in 2027. If not successful, it is possible the company will be purchased by SCHURTER at a bargain price—the supercapacitors are already branded.

My holdings: Due to a peculiar inertia and deep-seated fear of the regret I would feel if I am incorrect, I maintain a small holding against my better judgement.

Disclaimer: This article is provided solely for informational purposes and should not be construed as a personal recommendation, offer, or solicitation to purchase or sell any investments mentioned herein. Investors are advised to independently evaluate or seek professional advice to determine whether any transaction discussed is appropriate considering their investment goals, risk tolerance, potential benefits, and other relevant circumstances.

The views presented in this article are based on publicly available information, believed to be reliable at the time of publication. However, no warranty or guarantee, express or implied, is provided regarding the accuracy, completeness, or reliability of such information, and it is subject to change without prior notice. Opinions expressed reflect the judgment of the author at the time of publication and future outcomes may differ from statements provided herein.

The author has no business relationships or financial interests with any companies discussed in this article and has received no compensation from any third party related to the content produced

Bibliography

1 https://csiropedia.csiro.au/supercapacitors/

2 CAP-XX 2006 Annual Report: https://www.annualreports.com/HostedData/AnnualReportArchive/c/LSE_CPX_2006.pdf

3 RNS 2726V: https://otp.tools.investis.com/clients/uk/capxx_limited/rns/regulatory-story.aspx?cid=1213&newsid=573652

4 RNS 8178S: https://otp.tools.investis.com/clients/uk/capxx_limited/rns/regulatory-story.aspx?cid=1213&newsid=687872

5 https://www.eenewseurope.com/en/murata-sells-its-supercapacitor-lines/

6 https://otp.tools.investis.com/clients/uk/capxx_limited/rns/regulatory-story.aspx?cid=1213&newsid=1355018

7 CAP-XX Annual Reports, 2020-2024.

8 RNS 5401C: https://otp.tools.investis.com/clients/uk/capxx_limited/rns/regulatory-story.aspx?cid=1213&newsid=1553104

9 RNS 6633J: https://otp.tools.investis.com/clients/uk/capxx_limited/rns/regulatory-story.aspx?cid=1213&newsid=1807160

10 RNS 5477V: https://otp.tools.investis.com/clients/uk/capxx_limited/rns/regulatory-story.aspx?cid=1213&newsid=1406973

11 RNS 0705X: https://otp.tools.investis.com/clients/uk/capxx_limited/rns/regulatory-story.aspx?cid=1213&newsid=1742889

12 RNS 5045K: https://otp.tools.investis.com/clients/uk/capxx_limited/rns/regulatory-story.aspx?cid=1213&newsid=1880852

13 RNS 8738H: https://otp.tools.investis.com/clients/uk/capxx_limited/rns/regulatory-story.aspx?cid=1213&newsid=1802016

14 RNS 3243Y: https://otp.tools.investis.com/clients/uk/capxx_limited/rns/regulatory-story.aspx?cid=1213&newsid=1685343

15 RNS 1038O: https://otp.tools.investis.com/clients/uk/capxx_limited/rns/regulatory-story.aspx?cid=1213&newsid=1889119

16 RNS 3306X : https://otp.tools.investis.com/clients/uk/capxx_limited/rns/regulatory-story.aspx?cid=1213&newsid=1909701

17 RNS 5881O: https://otp.tools.investis.com/clients/uk/capxx_limited/rns/regulatory-story.aspx?cid=1213&newsid=1719646

18 RNS 6191X: https://otp.tools.investis.com/clients/uk/capxx_limited/rns/regulatory-story.aspx?cid=1213&newsid=1845771

19 RNS 5593W: https://otp.tools.investis.com/clients/uk/capxx_limited/rns/regulatory-story.aspx?cid=1213&newsid=1842885

20 RNS 9239V: https://otp.tools.investis.com/clients/uk/capxx_limited/rns/regulatory-story.aspx?cid=1213&newsid=1740510

21 https://www.rsm.global/australia/insights/state-play-strategic-rd-review-commences

22 RNS 3321T: https://otp.tools.investis.com/clients/uk/capxx_limited/rns/regulatory-story.aspx?cid=1213&newsid=1900797

23 RNS 3903I: https://otp.tools.investis.com/clients/uk/capxx_limited/rns/regulatory-story.aspx?cid=1213&newsid=1875517

24 RNS 4759I: https://otp.tools.investis.com/clients/uk/capxx_limited/rns/regulatory-story.aspx?cid=1213&newsid=1943230

25 Yaseen et al. (2021). A Review of Supercapacitors: Materials Design, Modification, and Applications.

26 https://www.gminsights.com/industry-analysis/supercapacitor-market

27 https://otp.tools.investis.com/clients/uk/capxx_limited/rns/regulatory-story.aspx?cid=1213&newsid=1835055

Appendix I

Prices in dollars. Not all pages were saved by the WayBack machine (marked with ‘X’) and so revenues from these lines are not included. Depending on starting stock levels, calculated revenues could be a significant underestimation. However, having kept an eye on stock levels since Feb 2025 it does not seem like these lines are rapidly selling, and so large sales between July 2024 and Feb 2025 would be surprising. This will ignore any re-stocking between July 2024 and May 2025 if it occurred. There may not be a 1:1 mapping between DigiKey stock levels and units sold.

Appendix II

CAP-XX Product and Competitors

To make a sound investment, you need to understand the business. To understand the business, you need to understand their product. Unfortunately for A$126 million in investor capital, supercapacitors are hard to understand. Nonetheless, we can look at the CAP-XX product line and use some key product specifications to get an idea as to where CAP-XX stands in the market.

Standard capacitors are ubiquitous in electronic circuits, with their cost in the order of a few cents. They are a poor store of charge (they have a low energy density) but can be rapidly charged and discharged (i.e. they have high power density, power being the rate of energy transfer).

Supercapacitors have much higher capacitance, power density and energy density (though their energy density is still significantly less than lithium-ion batteries). CAP-XX supercapacitors are Electric Double-Layer capacitors (EDLCs), an industry standard in which positive and negative electrodes interface with ionic solutions separated by an extremely thin membrane. This contrasts with standard capacitors, which typically separate charge with a dielectric material (e.g. ceramic).

Capacitor Specs

There are many key properties that a product design engineer must consider when designing an electronics product. A full analysis and comparison of the full specification sheet is far beyond my expertise (I am not an electrical engineer), however we can use a set of key parameters to get a sense of where CAP-XX products stand with respect to its competitors.

These are the capacitance (measured in F, farads), the voltage (typically in the range 2.5 to 5.5) and the equivalent series resistance (ESR). As energy stored goes with the square of the voltage (E = ½ CV²) increasing voltage is important for energy density (and not trivial, as ionic EDLC typically break down at higher voltages). The ESR in contrast is more important for charge and discharge times. Therefore, a product engineer will consider many factors, including size, depending on their use case.

Prismatic Lines

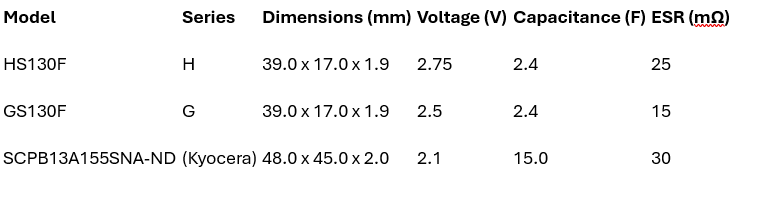

The first lines of supercapacitors CAP-XX produced, way back even before 2006, are the G-series (2.5 V) and H-series (2.75V) which are still sold today, in the price range $15-$20 (all prices quoted here are for a single piece, typically discounted for bulk orders).

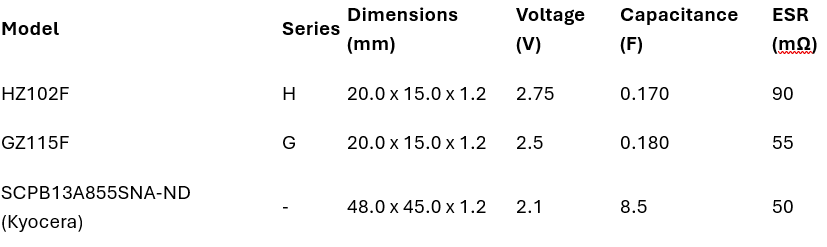

The main competition for the G- and H-series comes from Kyocera’s PrizmaCap range, which are wider in size but offer significantly larger capacitance. Below we take just the thickest and thinnest supercapacitor from the G- and H- lines and compare to a similar-sized Kyocera piece. In general, CAP-XX pieces are smaller, with significantly lower capacitance but higher operating voltages.

In addition to the G- and H- series are the ex-Murata lines, including the DMH. This is the ‘world’s thinnest supercapacitor’ at 0.4 mm thick. There is only one competitor in its class, Linga Energy’s (42 x 30 x 0.5 mm) thick S-Power supercapacitor, at 1.2F, 2.7V and 50mOhm ESR at $14 against CAP-XX’s (20 x 20 x 0.4 mm) thick, 35 mF 4.5V and 300 mOhm DMH around $13. Again, we see that CAP-XX prioritizes smaller form and higher operating voltage at the cost of lower capacitance.

Coin cell and supercapacitor

To broaden their range, in 2017 and 2022, CAP-XX released their coin cell and cylindrical range respectively, typically these are in the range of $1 per component. Here, the market is extremely crowded. This excellent article gives some insight into how crowded the market was in 2013:

https://www.tti.com/content/ttiinc/en/resources/marketeye/article/me-zogbi-20130403.html?srsltid=AfmBOorH5mDO0kP2NlI__k4ln4dBd7FLoVbatbNLmSvliGp7e_Be59y5

Prismatics are a much nicer subsection of this much larger, crowded market.

For example, of the 3000 supercapacitors on DigiKey around 2800 are coin cell or cylindrical. Take the CAP-XX coin cell 11 mm diameter by 4.5 mm height, 220 mF capacitance with 40 Ohm (note Ohm not mOhm) ESR, $0.87 for 2500 units. There are 113 coin cell supercapacitors in the 11-12 mm diameter range for producers such as Eaton, Sruite, KEMET and Elna America. Having a cursory look, it does seem that CAP-XX is competitive on price for its coin cell units and has good specs. These are again in the small capacitance range (0.22 – 1.5 F).

Other Lines

CAP-XX also produce 3V prismatic range, as well as lithium-ion supercapacitors.